You have a thriving business with clear strategic objectives in place, the right people by your side and a well-managed portfolio of projects. Congratulations, everything is ticking along nicely. Imagine that suddenly, utterly out of the blue, something changes that disables you from moving forward, totally disastrous! This could be a medical emergency for your most valued employee, forced office closures beyond your control or a significant drop in revenue due to external factors. You may have experienced one if not all of these over the past year.

We can provide you with the key elements that contribute to a strong contingency plan. Here are our top tips on what to include and how to best prepare when disaster strikes!

- Make a list of your crucial resource requirements:

Review your business and list the key resources you cannot trade without. This could range from your employees to facilities or key systems/tools. Make sure you prioritise or adjust your resource model if you can. Single points of failure should be avoided at all costs.

- Define key risks:

Figure out where you are exposed and define what the risk is to your business. Ensure when you are risk assessing that you consult with the experts in your business and fully understand what this means. In other words, what is the impact? Impacts could be cost constraints, reduced quality of work or mean an elongated time period is needed to complete crucial tasks. Whatever the risk, you must understand the impact so you can start put measures in place to counteract these risks. In other words – your contingency plan!

Top tip: when considering risks think about these categories: time, cost, resource, environment and technical.

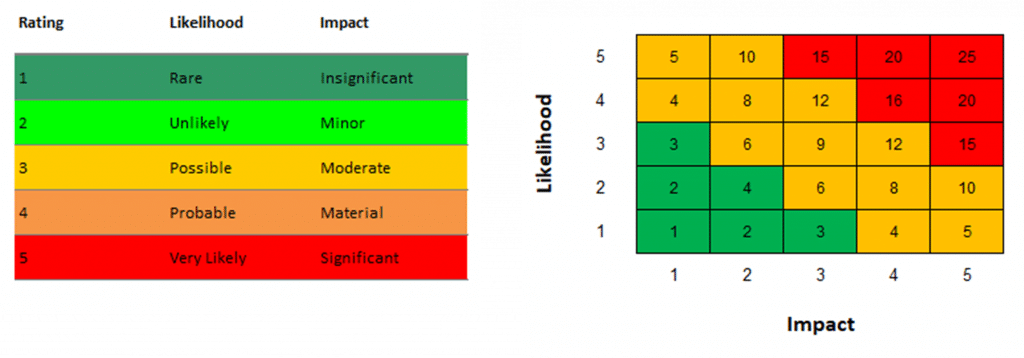

- Prioritise your risks:

After you have identified all the possible shortfalls, prioritise them to understand the key risks. An easy way to do this is to score the impact (1-5) of the risk along with the likelihood (1-5) and add this score together (out of 25). Have a look at our tried and tested scoring system below:

- Create a detailed contingency plan based on the risks identified. Use this formula

Now we’re getting to the crux of it. You have identified all the risky areas in your business and where your progress could be derailed; the next step is detailing your plan for every eventuality (almost)!

- Scenario planning: Using your highest priority risks list the most likely/impactful scenarios that could occur. Include a broad range of scenarios for example cyber attacks or IT malfunctions, long term employee unavailability, access to buildings/people/documents etc.

- Review the cause: Pinpoint specifically what will put your contingency plan into action. If you lose availability of a staff member is it a problem if they are off for four weeks or four months. Be specific!

- What is your action plan: Come up with what you will do and what actions need to be set in motion to respond to this event effectively. This will help individuals involved understand what, why and how they will execute the next steps.

- Who do you need to talk to? Decide on the individuals who will need to be informed of what is happening. This could include a wide range of stakeholders, the project team, sponsors, employees, customers, the general public. Tip: enlist someone in each scenario who can communicate issues appropriately and react well in a crisis.

- What do I need to do and when? Understand who is responsible for each aspect of the plan. RACI models are helpful – per activity decide who is Responsible, Accountable, Consulted and Informed. Lastly, think about when each activity needs to happen, is it in the first hour, day, week of the action plan happening? The detail of these will be dependent on the solution. Top tip: it is useful to give a rough timeline of when you think you will be able to resume normal business and creating criteria for how you will know it will be possible.

- Share your plan and keep it live!!

Now that you have your plan and understand fully the risks at that moment in time – do not file it away never to be seen again. Ensure you are continually reviewing your plans and evaluating the likelihood of risks being realised. Your business will never be in a static position and neither should your contingency plan. Assess how your business is changing and what measures you have in place to prepare for these.

We have seen this year how best-laid plans can come unstuck through nobody’s fault. At Nine Feet Tall we are experienced in delivering Contingency Plans, Risk Management, Scenario Planning and Business Continuity. For more information or a free consultation, contact EstherM@NineFeetTall.com